Eurozone Under Pressure: The Inflationary Spillover from the Iran Conflict

- Gabriel Gutanu

- Apr 23

- 7 min read

Inflation in the Eurozone has surpassed the ECB’s 2% target, reaching 2,5%. The increase was driven mainly by higher energy prices and was smaller than markets had expected. Still, trade disruptions caused by the closing of the Strait of Hormuz are pushing up fuel costs for European consumers.

“The war in the Middle East is creating the largest supply disruption in the history of the global oil market”. This is how the International Energy Agency described the effects of the closure of the Strait of Hormuz. However, the strait is not only an important transit route for oil and gas, but also for refined petroleum products, petrochemical feedstock, fertilizer and agricultural inputs, and broader industrial goods.

Sectors impacted

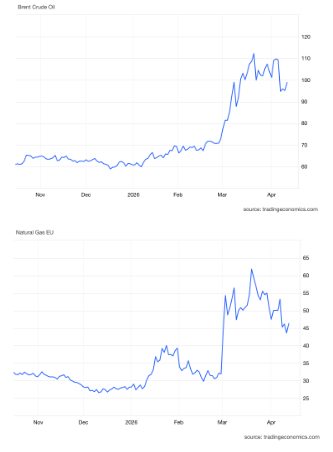

Oil & Gas

The Persian Gulf, and its outlet to the open sea, the Strait of Hormuz, is home to the production and (pre-war)transit of almost a quarter of the world’s oil and LNG. Following the beginning of the conflict, Iran closed the strait with the goal of gaining leverage against the US and Israel, and as a way of retaliating against their attacks, by laying naval mines and deploying Revolutionary Guard naval units that threatened to fire on or seize any ships transiting. Although there have been negotiations for a ceasefire beginning with April, passages have remained at around a 10-15 a day crawl, far from the pre-war norm of over 100 daily transits.

As a result, Brent crude oil prices surged to a high of $119-$126 per barrel, with gas prices in Europe reaching a peak of €62/MWh, but which has recently fallen slightly. After the beginning of negotiations, the Brent crude oil fell to the $100 mark, and EU gas prices stabilized around €44/MWh. Despite this fall, the bloc's heavy reliance on energy imports continues to pose significant challenges. The EU is especially vulnerable in imports of gasoline, diesel and jetfuel, caused by a loss in refining capacity. The ECB Energy Inflation indicator rose to 4,9%, and average prices at the pump for gasoline rose by 15% and 26,2% for diesel.

About half of the EU’s energy is procured by imports, with fossil fuels making up around 90% of them. The bloc's LNG has been primarily imported from the US, Qatar, Russia, Algeria, Nigeria and Norway. Following the closing of the Strait, Qatar halted LNG production following Irani strikes on their gas infrastructure.

France, the Netherlands, Italy and Belgium are some of the most exposed EU members to Qatari LNG imports. While Eastern Europe is less vulnerable to the price shock, they still remain affected . Despite some voices calling for the resumption of Russian gas imports, European Commission President, Ursula Von der Leyen stated that such an act would be a “strategic blunder”.

Fertilizer and food security

The strait is not only an important transit way for oil and gas, but also for fertilizer, with 30% of global supply passing through it. The Gulf region supplies even more of the world's most used nitrogen based fertilizer, urea, with 46% of global production originating in the region. While European countries do not mainly depend on fertilizers from gulf countries, the United Nations Food and Agriculture Organization(FAO) predicts a 15-20% increase in global fertilizer prices. FAO Chief Economist, Máximo Torero, stated that “Farmers are facing a dual cost shock: they have more expensive fertilizers alongside rising fuel costs affecting the entire agricultural value chain, including irrigation and transport,”.

While ECB figures show that food and non-alcoholic beverages remained at a steady rate of inflation, 2,4% in March, it will take time for the effects of increased shipping costs, and supply chain disruptions to reach the consumers. According to FAO, markets could stabilize in the next couple of months, if a solution is found swiftly. However, if the blocking of the passage progresses for a period longer than 3 months, it will have negative effects on the 2026-2027 growing season. In such a case, ECB data suggests that consumers would see a noticeable pickup in prices in the second half of 2026, continuing to 2027.

Manufacturing and Industrial Production

European firms face sharp increases in feedstock costs, especially for gas and methanol based intermediates. Added on top of increased energy prices, companies are facing tighter margins, which could lead to an industrial slowdown. The ECB has already lowered GDP growth forecasts by 0,3% for 2026 and 0,1% for 2027.

Despite limited European reliance on chemical feedstocks from the Middle East, Methanol prices rose by 23%. This rise, in spite of the fact that Europe imports just 8% of its Methanol from Oman and Saudi Arabia, can be attributed to increased spot trading, as producers sell their natural gas stocks. Methyl methacrylate (MMA) prices rose by 6,8%, and Acetic Acid prices by 10,6%, caused by Middle Eastern dependence and delays in shipping. Polyethylene producing firms faced increased losses. Naphtha-based High Density Polyethylene margins halved, from –€431/tonne in February, to -€885/tonne in March. Similar figures can be seen for other plastics such as LDPE and LLDPE.

With these feedstock margins collapsing, producers are likely to try and transfer some of these costs to industries down the value chain. This could mean increases in costs for plastic packaged food, household products, electronics and car components. Sustained price pressure in plastics and chemical intermediates would make a quick fall in inflation more difficult, even in the case of normalizing energy prices.

Another important product of the Gulf, Helium, is a critical coolant for advanced semiconductors, is essential for energy-grid modernization, electric vehicles, digital infrastructure, and defense systems. Qatar is the world's second largest helium exporter, producing 34% of global supply, largely as a by‑product of LNG liquefaction. Although such a share in production is very significant, overproduction preceding the war has lowered supply by only 10-15% for the time, though this situation is highly dependent on the length of the crisis. In a prolonged conflict, the aforementioned industries will likely face an increase in input costs, driving up inflationary pressure.

The war’s inflationary effects are self reinforcing. The increase in input costs are passed by producers to downstream industries, which become embedded into contracts. This makes it harder for inflation to redress, even in the case of a fall in energy prices.

The response

ECB

As European businesses face the macroeconomic situation caused by the conflict, the economic perspective in the EU changed from solid economic growth and stable inflation, to a new state of uncertainty. ECB President, Christine Lagarde, noted that the ECB has “a strategy that is built for a world of higher uncertainty”, ensuring that the European Central Bank can respond in a swift manner.

Although small energy shocks usually have limited inflationary impacts in the long term, she warned that more persistent shocks, such as the one in 2022, can have an inflated impact.

However, compared to 2022, the macroeconomic climate is in a calmer state, with near target inflation, and neutral fiscal policies. In addition, factors that positively impact the pass-through of energy shocks such as higher inflation and tight laboir markets are less prevalent.

The ECB has 2 scenarios for the impact of the conflict: an intensified but short lived shock, and a longer and broader shock. Regardless of scenario, inflation is expected to rise, by 1% in 2026 in the first case, but falling back by 2028, and 3% for the second case, with inflation rising by 3% in 2027, without returning on target within the period projected by the ECB. While in the short term scenario, growth would decrease slightly in the next 2 years, it would recover in 2028. The long term projection sees noticeably lower growth in the first 2 years, before also rebounding in 2028.

Monetary response is dependent upon the length and impact of the shock. The ECB’s strategy is to implement a “forceful and sustained monetary policy” in the case of a significant deviation from its inflationary target, in order to avoid deviations becoming cemented.

As of April, the ECB has not changed its main refinancing rate, which remains at 2.15%, with the deposit facility at 2.0% and marginal lending rate at 2.4%.

Government responses

In early March, 20 EU countries contributed 92 million barrels to a 400 million oil barrel release by the IEA, in order to mitigate the effects of the closing of the Strait. This however is a temporary measure, and these reserves, which are expected to last around five months, are already in use. In the case that the crisis lasts for a prolonged period, Energy Commissioner Dan Jørgensen stated that the bloc “will not rule out another release”.

In order to address the increase in energy bills, the EU Commission is considering a tax on excessive profits made by oil and gas companies. Modeled after the 2022 EU Solidarity contribution, these “windfall profit taxes” helped the most vulnerable countries cope with soaring energy prices following the Russian invasion of Ukraine and if implemented, they could increase revenues by €51 billion.

In a similar vein, Italian Prime Minister Giorgia Meloni, suggested a temporary suspension of EU budget deficit rules, if the conflict prolongs. In Italy’s case, the conflict's effects complicate its effort to ensure that its budgetary deficit goals are met. Her government is one of the most supportive of “windfall taxes”, and is prepared to introduce price cap measures on energy prices.

The crisis also highlighted the urgent need for Europe to take action in addressing inflationary pressure with more than temporary measures by decoupling from volatile energy suppliers, moving towards a future of reliable, safe, and most importantly european energy. Through the REPowerEU Plan, the EU has channelled more than €200 billion in renewables and supporting energy infrastructure. Since 2021 the share of energy production from renewables went from 37,8% to 48% in 2024. By accelerating the use of green hydrogen for industry and transport, the EU has cut reliance on Middle Eastern Oil and Qatari LNG by a third since 2021, with Spain and Portugal, which generate approximately 50% of their energy from renewables, seeing the least price volatility for consumers.

The Iran war may be the beginning of a new wave of inflation, not just because of the energy prices, but also from disrupted supply chains and disrupted agricultural seasons. Although the release of oil reserves may buy some time, the other industries affected by the conflict could push inflationary pressure even higher. While the ECB and EU governments are actively monitoring the situation it remains to be seen if the bloc has really learned the lessons of the 2022 energy crisis.

Comments